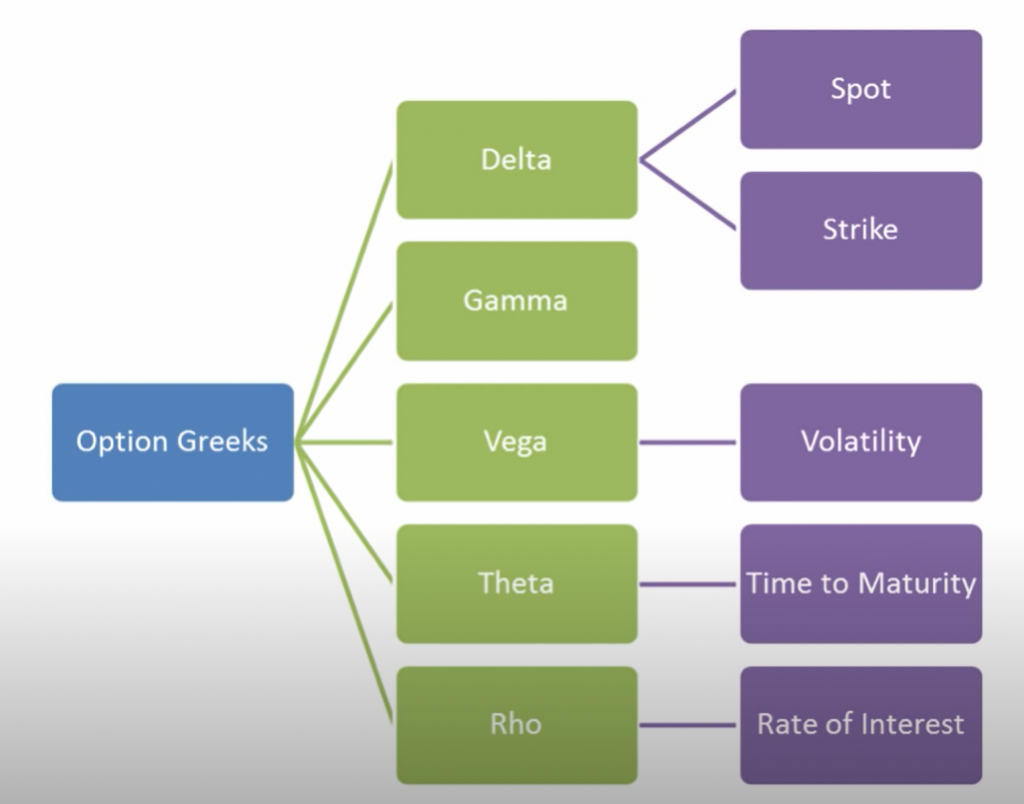

Delta, Gamma, Theta, Vega – the Greeks

Delta: the option value change per contract when the underlying security increase by 1%.

Gamma: the change rate of delta when the underlying security price changes.

Theta: the value you lose per day when it comes to the expiring date.

Vega: The amount the price of put or call will change for every 1% change in implied volatility.

Implied volatility is the only unknown factor in the option pricing. This is where the Edge for the option seller comes from.

IV is calculated by the current market activity, using the Black-Scholes formula.

American style option can be exercised anytime before expiration whereas European style option can only be exercised at expiration.

Standard U.S. equity options (options on single-name stocks) are American-style. Options on stock indices such as the NASDAQ (NDX), S&P 500 (SPX), and Russell 2000 Index (RUT) are European-style.

Also, equity options are not cash-settled—actual shares are transferred in an exercise/assignment. Broad-based indices, however, are cash-settled in an amount equal to the difference between the settlement price and the strike price, times the contract multiplier.

Option styles and settlement