会计学的目的是记录公司的资产,和总结每一笔交易,并反映在账目上。它有点像公司的体检表,表明公司的健康程度。

公司的体检表有三张:资产负债表balance sheet,现金流表statement of cash flow,收入表income statement

需要指出,accounting的财务报表也分为三种:financial accounting(为外部投资者所准备),Tax accounting(为报税准备),Managerial accounting(为内部决策准备)。

SEC: The Securities and Exchange Commission. 证监会

上市公司根据证监会的要求,准备年度报告(10K),季度报告(10Q),实时报告(8K)(当重要事件发生时)。

有趣的是瑞幸咖啡自爆造假的report却是6K而不是8K

本笔记着重讲US financial accounting的要求。

与日常生活中一手交钱,一手交货的交易方式不同。公司进行的交易包括了借贷,钱货不同时进行等复杂的情况,这需要独特的记账技巧。

谁准备财务报表?

上市公司自己准备财务报表。公司管理层,公司股的财务顾问,GAAP,媒体,分析师会监督上市公司的报表。作为投资者的你自己也要学会读财务报表。

财务报表的组成

Balance sheet:financial position of the company at a specific time。某一时刻,公司的财务状况。

Statement of cash flows: 现金流表单。物理上从时间A到时间B,流入与流出你账户的钱。

Statement of stakeholder’s equity

Income statement: 分为revenue 和 expense。它把你的投资支出(比如租房)平摊到每个月里,最后revenue – expense = net income。注意net income != change in cash。因为net income还包括你没收上来的客户钱,也包括你提前支出的钱,也减去了你压着的上游供应商的钱。(这段时间里你账面上(并不是钱包里的cash)赚了/赔了多少钱)

注:net income假设借贷,租赁,销售的合同都会生效并如期执行。

其实就个人而言,你也可以给自己做出这三张表

资产负债表:

你的银行账户余额+投资账户余额+车的价值+房子的价值=剩余房贷+剩余车贷+股东权益(这项是为了平掉这个等式)

现金流表:

直接看你这个月月末的银行账户余额 – 上个月月末银行账户余额

收入表:

W2收入+投资收入 – 房贷支出 – 生活支出

cashflow statement分为operation, investing 和 financing.

operation指公司的业务经营所带来的现金流,比如出售商品或服务。

investing指公司的投资所带来的现金流,比如买地买设备。

financing指公司的借贷所带来的现金流,比如借债,还利息,分红。

Balance sheet equation

Assets = Liability + stockholder’s Equity

Resources = Claims on resources by outsiders + owners.

Balance sheet永远是相等的。

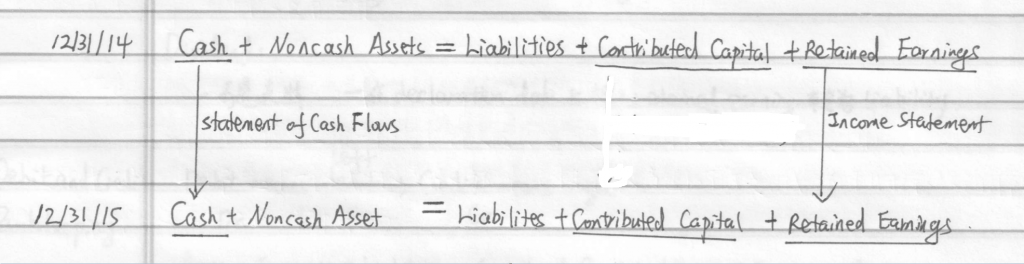

如何理解这三张表的关系?

如上图所示,14年年末和15年年末我们都制作了一份资产负债表,那么两个时间点之间的Cash的diff就是cash flow表;retained earning的diff就是income statement。

Stockholder’s equity = contributed capital + retained earnings

retained earnings = prior retained earnings + net income – dividends

asset = liabilities + contributed capital + prior retained earnings + net income – dividends

什么是Asset?

Asset is a resource that is expected to provide future economic benefits. (Generate future cash inflow or reduce future cash outflow)

- It is acquired in a past transaction or exachange

- The value of its future benefits can be measured with a reasonable degree of precision

比如:预付的房租,购买的机器,土地,货物已发出但还没收缴的货款(account receivable),都属于Asset。

资产是能够生钱(或省钱)的东西,由交易获得。比如你买了一辆车,如果车用于做Uber,那么这个车是资产(投资)。如果这车用来个人使用,那么这车就不是资产(消费)。

什么是Liability?

Liability is a claim on assets by ‘creditors’ (non-owners) that represents an obligation to make future payment of cash, goods or services.

- The obligation is based on benefits or services received currently or in the past

- The amount and timing of payment is reasonably certain

Liability(责任,义务)是公司收到了好处,但还没给钱,钱数可控。比如,用户在年初付了Youtube一年的会员费。Youtube收到了这笔钱,但需要一年的时间持续为用户提供服务。那么在年初,用户付钱的那一刻,所有的会员费都是Youtube的liability。这个liability随着时间的推移,随着Youtube为用户提供会员服务,会逐渐减少。

什么是Stockholder’s equity

stockholder’s equity也叫book value, net worth, net assets. 指公司股东所拥有的净资产。

= Assets – Liabilities

- contributed capital 卖原始股募集的资金

- retained earnings_end = retained earnings_begin – dividends

Dividend不是支出,在declaration date时把retained earning转为liability。

Debit and credit bookkeeping

Debit (Dr.) means left; Credit (Cr.) means right

account分为Asset account和Equity,liability account。

asset account在等式的左边;equity,liability account在等式的右边。

与资产负债表类似,等式左边表示资产,等式右边表示对资产的所有权claim。

Asset + expenses = Liabilities + contributed capital + Retained earnings + revenues

debit asset account 增加金额

debit liability/equity account 减少金额

credit asset account 减少金额

credit liability/equity account 增加金额

为什么要用debit credit bookkeeping记账法?

这篇文章和这篇知乎讲的很好,简而言之:单式记账法只能记录自己账户的收入支出,无法记录诸如借贷、转账、定金、报销等交易。并且,单式记账难以核实是否漏记,多记等情况。

复式记账法不仅记录了钱进来了/出去了,还记录了钱从哪里来/流向了哪里。

复式记账法的局限性是什么?

Bookkeeping Reference: https://bench.co/blog/bookkeeping/debits-credits/

Revenue and expenses (Accrual accounting)

Revenue: an increase of shareholder’s equity (not necessarily cash) from providing goods or services.

成为revenue的两个条件

- It is earned (good s or services are provided) and

- It is realized (支付的货款可以用金钱来衡量;钱转账了)

Realized了但是没有earned的例子:健身房卖出一张一年的健身卡,$100。这里的$100记作cash inflow,会出现在cash flow statement上,因为物理上这$100已经打到了你的帐上,叫做advance payment(预付款)。但它不能记为revenue,因为健身房还没有为客户提供一年的服务。这里的revenue可以按照每月$100/12的速度平摊到每月的收入上。

Earned但是没有realized的例子:公司在客户还未付钱时,先把货物寄送出去,这个transaction earned但是没有realized。

货款先到了,但是服务/商品还没给客户,叫做deferred revenue。它是公司的liability。

服务/商品给客户了,但是货款还没到,这是accrued revenue。它是公司的asset。

Exception

有时候,即使earned了,也realized了,这笔交易也不能记作revenue。比如Amazon允许客户在一定期限内退货退款的policy。这种情况要等退货期过去了,或者减去退货rate的estimation后,才能记作revenue。

联系:小明3月份时在Delta订了一张5月份的机票,花了$500。假设小明5月份乘机的话,请问这$500元:

1. 是否出现在Delta 3月份的income statement上?cash flow statement上?

2. 是否出现在Delta 5月份的income statement上?cash flow statement上?

假设小明4月份,cancel了ticket,并且拿到了full refund。那么Delta 4月份的income statement和cash flow statement如何反映这笔$500?

Expenses: decrease of shareholder’s equity that arise in the process of generating revenues.

expense分两种:

- product cost: 商品的材料成本

- period cost:商品的行政成本(管理人员工资,销售,开发)

当revenue被记上时,相关的expense(product cost)也要记上。

当revenue没被记上时,period cost也要记上。

Accrual accounting是保守的,只有revenue earned/realized了才记账;只要expense被预估了会发生,就要计在帐上。

比如预计要付的税款,Google预计EU会罚它的罚款,都会提前写在expense里。

传统商业模式,比如卖商品,product cost很好计算。比如苹果生产一部手机,product cost就是它所有原材料的成本。但广告商业模式,product cost就没那么直观。

Google的计算方式里,ads的product cost是TAC (traffic acquisition cost)。比如它支付给苹果的流量入口费,它支付给内容提供商的内容费。

Adjusting Entries

在财务周期的末尾,我们记下了很多的transaction。现在需要加入新的transaction来反应deferred expenses/revenues 和 accrued revenues/expenses。这些transaction都是internal transaction。

比如在这个记账周期内,是不是逐渐产生了一些费用/收入,但是还没有记账?prepaid rent (asset -> expense) ; Salaries and wages payable; Income taxes payable; Depreciation and Amotization 资产折旧。这里的折旧率 = (购买价 – 作废价) / 使用年限。作废价和使用年限都是公司根据市场行情而定。

注意:当资产中的房价上涨时,我们不记在账上,因为记账要保守。(这里其实是记账的不准确性了)此外,只有房子会折旧,土地不折旧。

Balance sheet中的收入和支出不会一直增长下去,在close entry时,把收入和支出汇总到retained earning里。

Financial Statements and Closing Entries

把Entries 在上一步调节好后,先做Income statement 再用Net income去更新retained earnings来做balance sheet。最后一步完成statement of cashflow和statement of shareholder’s equity。

Income statement format

Gross profit (毛利润) = Revenue (or sales) – cost of goods sold (product cost)

Operating Income(公司核心业务的收入,最为关键的一行) = Gross profit – operating (SG&A) expense

Pretax Income = Operating Income -(+) interests, gains, and losses

Net Income(净利润) = Pretax Income – Income Tax expense

Balance sheet format

Assets: Assets are listed n the following order

- current asset (benefits within next year, ordered by liquidity以流动性排序)

- Cash

- accounts receivable

- inventory

- prepaid assets

- Non current assets

- tangible assets

- intangible assets

Liability and stockholder’s equity

- current liabilities (obligations within next year, ordered by liquidity)

- bank borrowings

- accounts payable and other payables

- deferred revenues and other noncash

- noncurrent liabilities

- bank borrowings and bonds

- other types of liabilities (deferred taxes, pensions)

- stockholder’s equity

- contributed capital

- retained earnings

Close Entries

最后,把所有的临时账户都关掉,比如expense和revenue。

Statement of cashflow format

现金因为运营、投资、借贷而产生的变化。

运营:顾客付款,给供应和三个付款,员工工资等。

投资:买卖资产

借贷:发新股,回购,借钱。

如果公司A借钱给公司B,那么这算是公司A的operating activity。不算financing activity。(但应该算是公司B的financing activity?)

如果投资支出比较大的话,公司可能在投资未来。一般来说,投资支出可以带来未来的收入现金流。如果account receivable 和 account payable都在增大,证明公司业务在扩张。

比例分析Ratio Analysis

用比例值进行同一公司的纵向比较,或同一行业,不同公司进行横向比较。

Ratio可以衡量一个公司的风险,流动性,盈利。

Ratio一定要与一定的benchmark进行比较,比如不同时间,同一个公司的数值,或者同一时间同行业不同公司的数值。

ratio are contextual,要去挖掘ratio背后的原因。ratio无法直接提供答案,但他会引导你问出正确的问题。

ratio可能会被公司管理者manipulate。

常见的ratio

Return on Equity (ROE) = Net Income / Average shareholder’s equity

他表示的是投资者的投资回报率,但没有考虑风险。

ROE有两个driver:

- operating performance

ROA = Net income / average assets = (Net income / sales) * (sales / assets)

ROA表示公司利用其资产赚钱的能力。

Net income / sales 是公司的利润率(profitability);Sales/assets 效率(efficiency)

- financial leverage

公司的负债杠杆率有多大

Financial leverage = avg asset / avg shareholder’s equity

所以当你看到ROE很大时,你要进一步看是ROA打还是Financial leverage大。ROA大是好事儿,Financial leverage大不是很好。

ROE = ROA * Financial leverage

= net income / asset * (asset / stockholder’s equity)

= (net income / sales) * (sales / asset) * (asset / stockholder’s equity)

= 利润率 * 资产利用率 * 杠杆

对于跳蚤商店等地段走量的店,利润率低,资产利用率高。

对于奢侈品店,利润率高,资产利用率低。

注意,以上的分析都跟股价无关。它分析的是公司的价值。

common size sheets

公司在增长,如何比较同一公司不同时间其的健康程度?

解决方案:

- 资产负债表:所有数字除以总资产(total asset)

- 收入表:所有数字除以sales

- 现金流表:不需要调整

实际上应该除以通胀率,按照constant dollar value 来算。

Key ratios profit margin analysis

Gross margin (毛利率) = (sales – cost of goods sold) / sales

search ads的毛利率是很高的,可以到80%甚至。因为它的direct cost只是TAC,data center的硬件,电费,网费。

SG&A as a% of sales = SG&A Expense / Sales

Operating Margin = Operating Income / sales

Interest Expense as of sales = Interest Expense / sales

Effective Tax Rate = Income Taxes / pre-tax Income

Assets Turnover Analysis

Days receivable = 365 * (Avg. accounts receivable / sales) 公司多少天才能收到货款

Days Inventory = 365 * (Avg. Inventory / cost of goods sold) 产品在库房里压多少天才能卖出去

Days payable = 365 * (Avg. accounts payable / purchases) 公司压供应商货款多少天

Net trade cycle = days receivable + days inventory – days payable 公司需要多少短期贷款才能维持运转

Liquidity ratio

流动性比例,他表示的是公司资金链断裂的风险。

Short term ratio (越大越好)

current ratio: current assets / current liabilities

但是,不是所有的asset都能转成现金。

quick ratio: (cash + receivables) / current liabilities

CFO to Current liabilities: cash from operations / avg current liabilities

Interest coverage ratios (公司有无能力支付贷款利息) (越大越好)

interest coverage = (Operating income before depreciation) / interest expense

Cash interest coverage = (cash from operations + cash interest + cash taxes) / cash interest paid

Long term debt ratios (公司是否会破产)

Debt to equity: total liabilites / total SE

Long term debt to equity: total long term debt / total stockholder’s equity

Long term debt to tangible assets: total long term debt / (total assets – intangible assets)